‘Productivity isn’t everything, but, in the long run, it is almost everything. A country’s ability to improve its standard of living over time depends almost entirely on its ability to raise its output per worker.’ (Paul Krugman, distinguished professor of economics at the Graduate Center of the City University of New York)

Investment and productivity are the engines of economic growth. Government policy influences investment and economic growth through taxation, spending and regulation. It creates the economic environment in which individuals and businesses operate. The government’s decisions about the nature, timing and level of taxation have an impact on productivity, as do its decisions about public spending on capital infrastructure, controls over the external supply of skilled workers, and investment in the skills of the workforce.

Impact of taxation

Taxation affects productivity by distorting the prices and allocation of the factors of production: land, labour and capital. It alters the rate of return expected from entrepreneurship and the incentive to undertake research and development (R&D). Corporate taxation influences private investment decisions by altering the net return from investing capital and the incentive to invest. High marginal rates of income tax reduce the incentive to supply labour. Taxation influences decisions by individuals about whether it is advantageous for them to enhance their human capital (their embodied education, training and marketable skills). Progressive taxation reduces the appetite for long-term investment, risk taking and entrepreneurial activity.

Taxation is but one of a range of factors that influence investment, productivity, and growth. Many of Britain’s trading rivals, such as Germany and France, enjoy higher levels of national income, productivity and growth, despite levying considerably higher corporate and personal tax rates. The reduction in corporate taxation and personal tax levels in Britain since 2010 have not led to increased investment and economic growth. They have simply increased share prices and exacerbated wealth inequality. The reduction in the government’s own spending on capital investment that accompanied the tax cuts has damaged productivity and growth.

Why productivity matters

‘Productivity is one of the most important indicators of a strong economy. It is ‘the key determinant of the economy’s potential growth rate, the rate at which the economy can grow without generating inflationary pressures, in other words its speed limit’ (Sir David Ramsden, deputy governor for markets and banking, Bank of England, 2018).

Labour productivity is measured as the value of goods and services that a typical worker produces each hour, i.e. the total value added in the economy divided by the total hours worked. There are other measures of productivity. Economic theory defines productivity as the residual of output that is not explained by the direct contribution of the factors of production. This residual is commonly referred to as ‘total factor productivity’.

Countries with strong productivity growth enjoy higher levels of real income, growth and low inflation. They also tend to have improved health indicators, because higher productivity allows workers greater scope for leisure.

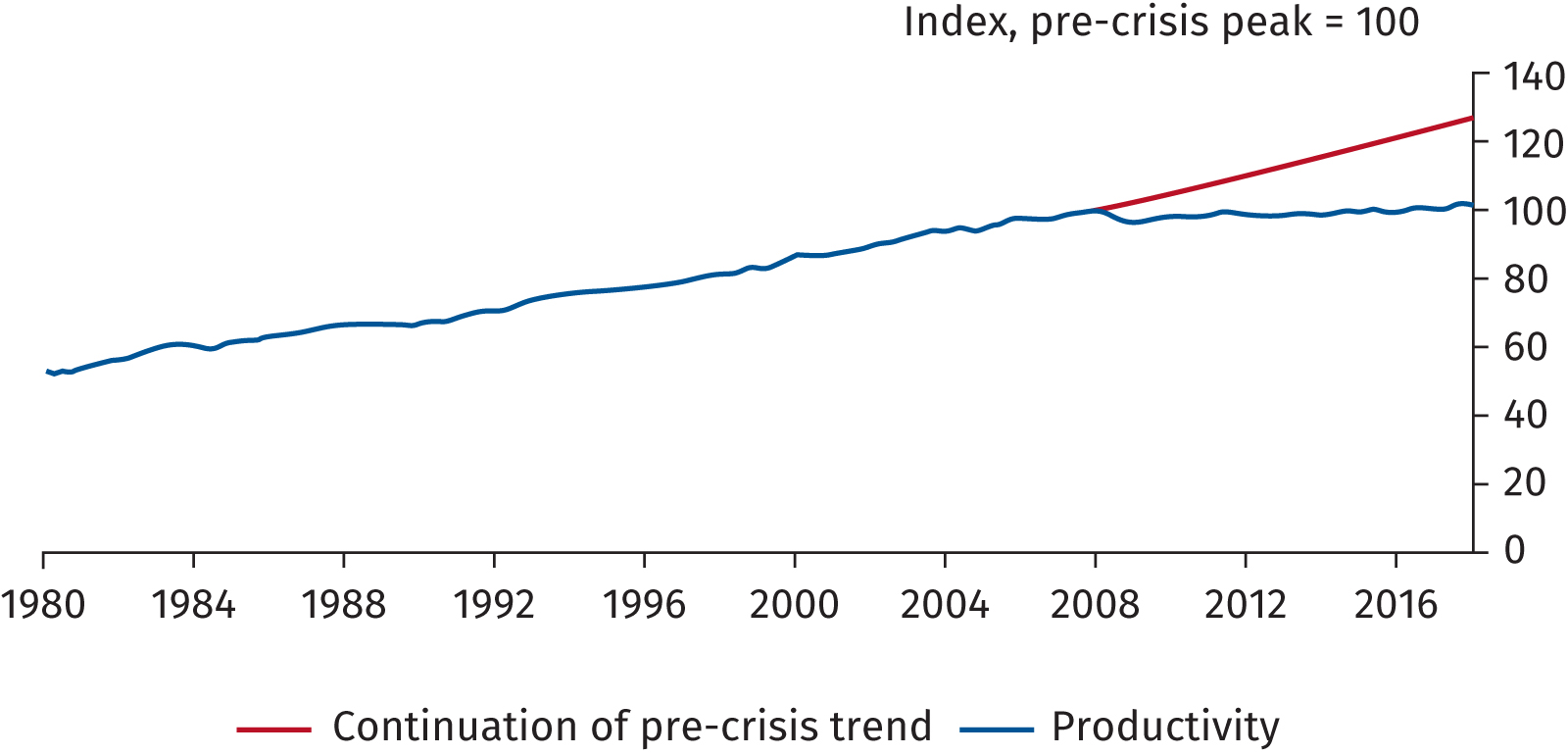

The enigma of Britain’s record levels of employment but stagnant real wages and sluggish economic growth is wrapped around the ‘productivity puzzle’ that has bedeviled economic policy makers since the financial crisis. Britain’s productivity fell significantly after the financial crisis in 2008. Other advanced economies suffered a similar dip. Puzzlingly, though, Britain’s slowdown has been larger and longer lasting than that in almost any other economy.

Productivity growth has largely recovered in the other advanced economies since the financial crisis, but Britain’s annual productivity growth has remained persistently weak. Productivity is running almost 20% below its former level, had it continued along its pre-crisis trend (see figure 1 below). Whereas ‘historically we have either been growing above 2%, or in or close to recession. We have little experience of this middle ground’ (Ramsden, 2018). Britain has remained in the economic doldrums despite the markedly business friendly fiscal environment since 2010.

Figure 1: UK productivity relative to continuation of pre-crisis trend

Sources: ONS and Bank of England calculations.

Notes: Productivity is output per hour worked. Extrapolation of pre-crisis trend based on continuation of average growth from 2007.

Why we need to take action

‘Productivity growth is a gift for rising living standards, perhaps the greatest gift… [T]ackling the... productivity puzzle is among the most pressing public policy issues today’…. ‘Productivity is what pays for pay rises. And productivity is what puts the life into living standards’ (Andy Haldane, Bank of England chief economist, 2017, 2018).

The weakness of Britain’s productivity growth explains why the record number of jobs in the economy has not been matched by their quality. Most of them are precarious, and real wages and living standards have stagnated.

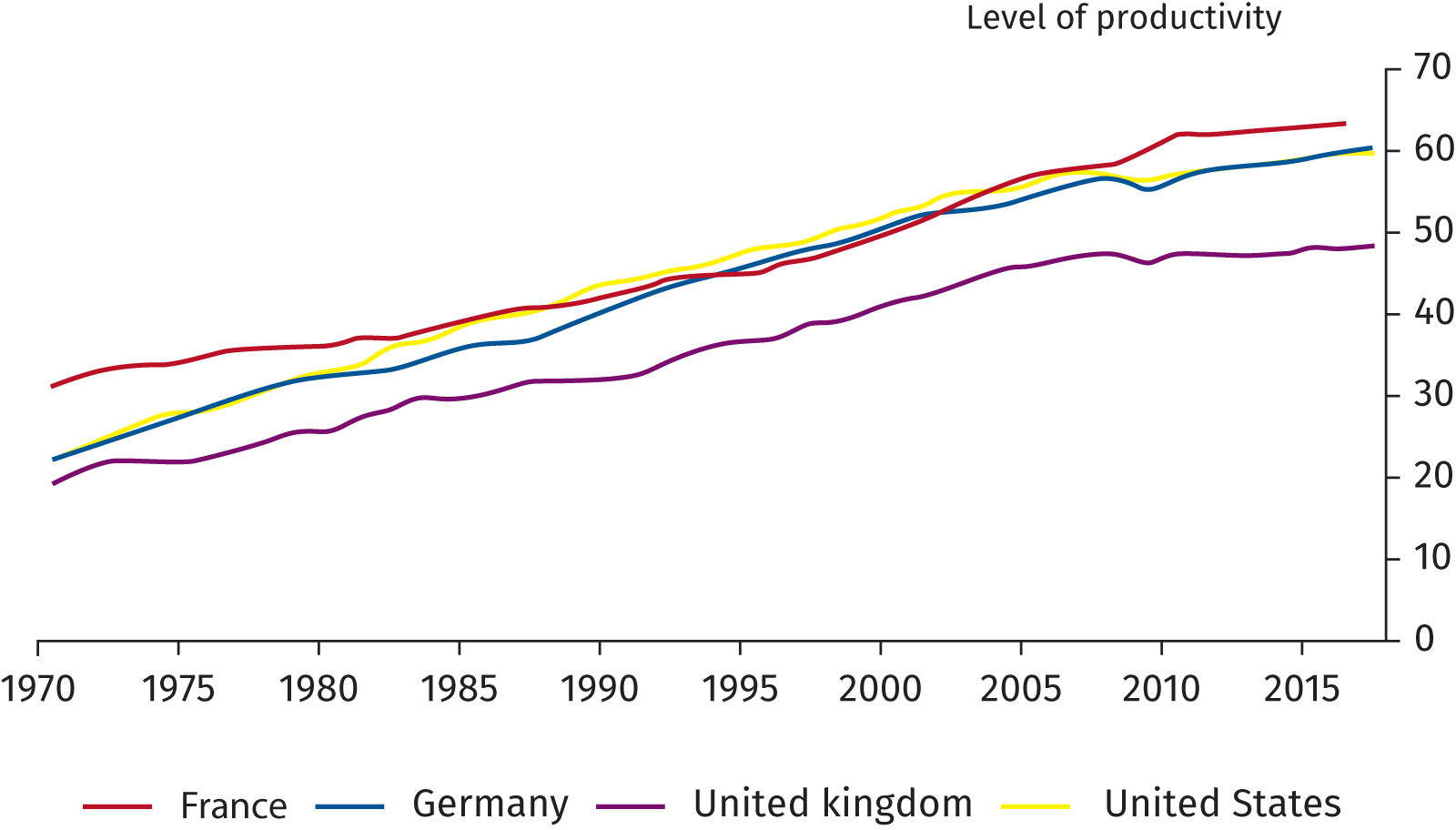

Britain was the most productive nation in Europe until the 1960s. It had a higher level of productivity than France and West Germany. Britain continued to grow, but it fell behind. It suffered the ignominy of being described as the ‘sick man of Europe’ until the market reforms introduced by Margaret Thatcher’s government revived British productivity. Britain’s annual growth rate was a relatively sprightly 2.3% before the financial crisis. It has been estimated that if Britain had continued growing even at the level of 2% a year, productivity would have been more than a quarter higher today.

Instead, we have again fallen behind the other advanced economies (see figure 2 below). The Office for National Statistics has estimated that labour productivity is, on average, 16% higher in the six other members of the G7 than in Britain. (US productivity is nearly 30% higher, and Germany is 35%.)

‘If British workers were able to catch-up to the G7 average, what currently takes us five days’ work to produce could be done in little over four. If we were able to catch up with Germany, we might all be able to go home from work on Thursday afternoon each week without any fall in GDP’ (Silvana Tenreyro, professor of economics, London School of Economics, 2018).

Figure 2: Productivity in UK, US, Germany and France

Notes: Productivity is output per hour worked in US$ at constant prices, using 2010 PPPs.

Determinants of productivity

Productivity is determined by:

Declining productivity is not a uniquely British phenomenon. Even before the financial crisis, productivity growth was sluggish in advanced economies in the period since 1970, following the period of exceptional growth over the previous century. In his monumental study of the rise and fall of growth in the US, Robert Gordon (2016) argued that the hundred years since 1870 represented a period of exceptional growth. It was a period during which there were unprecedented life-changing innovations. Gordon said that there was no reason to suppose that it would be repeated. The advanced economies may have entered an age of secular stagnation because of demographic trends and diminished rates of innovation; they might have to get used to permanently lower growth.

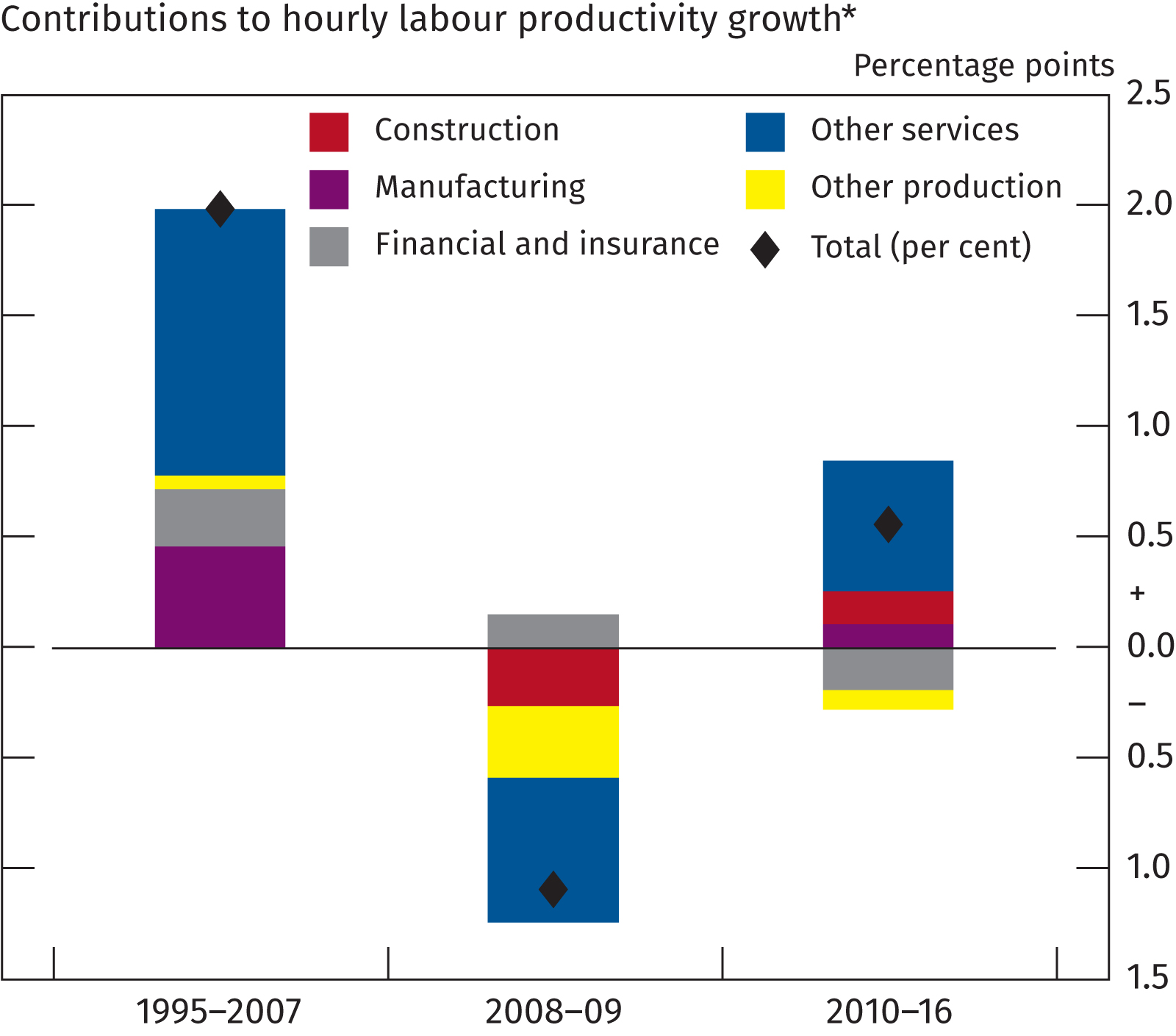

This does not explain why the levels and growth of British productivity have fallen behind that of its international peers. Indeed, Britain’s productivity gap with its fellow G7 members (other than Italy) has been increasing since 2007. Detailed analysis of the sector by sector industry contributions to labour productivity growth indicates that the finance and manufacturing sectors accounted for three-quarters of the fall in Britain’s aggregate productivity growth (see figure 3 below). (Ironically, the same sectors contributed about half of the UK’s productivity growth in the seven years leading up to the financial crisis.) The rest of the shortfall in productivity growth was accounted for by the information and communications technologies and professional, scientific and technical services sectors.

Figure 3: Sectoral contributions to productivity growth

Notes: Productivity is output per hour worked in US$ at constant prices, using 2010 PPPs.

Possible causes of the productivity gap

There has been no shortage of explanations for the stagnation of British productivity since the financial crisis. They include the suggestion that the financial crisis has somehow permanently ‘scarred’ the productive capacity of the economy. It has been claimed that the productivity puzzle is simply a ‘statistical mirage’. It has also been suggested that official statistics underestimate the level of economic activity and productivity gains in Britain’s services dominated economy, and particularly the impact of the pervasive diffusion of digital technologies across all sectors of the economy. In fact, the main reason for the weakness in labour productivity is the industry-wide fall in investment during the crisis and its slow growth afterwards.

Possible under-recording of income

The launch of platforms for transport and accommodation services such as Uber and Airbnb have turned many households into digital producers. The ready availability of high capacity computing power connected through fixed or mobile internet access services has also created opportunities for households to engage in profitable commercial transactions through unregistered platforms, social media and other informal channels that are not always reported to HMRC or measured as part of the GDP. Paraphrasing Robert Solow’s (1987) famous quip about computers, one can see the impact of the digital economy everywhere but in the productivity statistics.

Impact of loose monetary policy

Government policies such as quantitative easing and financial support for low productive ‘lame duck’ firms and industries have impeded what economist Joseph Schumpeter labelled the evolutionary economic ‘process of creative destruction’. This is the mechanism through which the capitalist system periodically clears out outmoded and inefficient firms and industries to make way for their more dynamic and innovative upstarts. There has been no such clearing out in Britain. Company failures have remained at a lower level than one would have expected given the size of the fall in the GDP in the wake of the financial crisis.

Interest rates have ceased to fulfil their role of providing finance primarily to strong and profitable performers. Quantitative easing has resulted in historically low interest rates, and the creation of a borrowers’ market. This has enabled companies that should arguably have gone to the wall to continue trading on borrowed capital. Zombie companies have low levels of productivity, and a significant proportion of them have seen no productivity improvements for decades. The continued survival of such companies results in long-term capital misallocation, and to lower aggregate productivity and lower long-term returns. They are a drag on productivity and growth, and sap the economy of dynamism.

The upper and lower tails

Britain has many innovative and highly productive companies. It is also renowned for the quality of its R&D and start-ups. But there is a wide variation in the degree of technological adoption and penetration among British companies. Some of them, the so-called upper-tail companies, are constantly on the look out for new talent, ideas and technology. They rapidly adopt new technologies and spread them equally quickly within the firm. They tend to be highly productive. They include the 400 large companies (less than 0.01% of the business population) that account for three-quarters of Britain’s private R&D spending, and other companies involved in exporting goods and services.

However, the long and lengthening lower tail of companies that have little or very low productivity have dragged down Britain’s aggregate productivity. About half of British firms have not experienced any increase in productivity since before the financial crisis. In some regions and sectors, the fraction of firms that have practically stood still since the turn of the century is almost two-thirds. Smaller companies tend to have a poor track record of innovation. They are often slow to introduce new products and processes. The poor performance of businesses in the lower tail goes a long way towards explaining why British productivity has stubbornly failed to recover since the financial crisis.

Knowledge diffusion

British industry is poor at disseminating and diffusing the innovation it is so good at generating. It is consistently in the top five for global innovation but Britain’s ranking for domestic knowledge diffusion is a poor 38th – and falling. Human capital is a powerful transmission and diffusion mechanism for channelling ideas and innovations within and across companies and countries. As people move between companies, they take their knowledge, expertise and experience with them and share it with their co-workers. Churn in the labour market tends to promote technological diffusion. The fact that it is about half the level in Britain than it is in the United States may partly explain why British workers are significantly less productive than those in the US.

Animal spirits

Most economists attribute the productivity puzzle to the collapse of investment during the crisis, and its gradual and only partial recovery since then. Economist John Maynard Keynes famously declared that a large proportion of our positive activities, such as investment, depend on spontaneous optimism which he referred to ‘animal spirits’.

‘The investment element of GDP is where the animal spirits of the economy bark first, and where a recession first bites’ (Haskell & Westlake, 2018). Investment also declined in other advanced economies in the wake of the financial crisis, but it has recovered there. If British industry had similarly continued investing in and adopting new and tested technologies and processes that enhance productivity, it is highly probable that Britain’s aggregate productivity growth would have rapidly bounced back to its former level (or beyond). Instead, business investment was unusually weak relative to past recoveries, even before the economic uncertainty created by Brexit.

Since 2008, investment has been far lower than in the recoveries that Britain experienced after the 1979 and 1990 recessions. The cumulative growth in business investment is still up to 50% below the equivalent stage of recoveries seen in the post-war recessions. The Bank of England recently estimated that the level of investment might be between 6% and 14% lower than it might have been because of uncertainty over the economic impact of Brexit.

Intangible assets

There is a strong correlation between investment in intangible assets and productivity. Investment into intangibles was affected to a lesser extent than tangible investment after the financial crisis, but it had a disproportionately large adverse impact on productivity. This is because intangible capital tends to produce higher spillover effects than tangible capital. Intangible capital is highly productive.

Intangible assets comprise ideas and know-how, intellectual property, software, licensing agreements, secret recipes, branding, proprietary relationships with suppliers and partners, and product design. Since the 1980s, the growth of investment in intangible assets has outstripped that of investment in physical capital, such as plant and equipment and structures. Even businesses in countries renowned for their ‘dark satanic mills’ of manufacturing are increasingly dominated by intangible capital.

Knowledge capital can be re-combined into new forms. It is easy to scale intangible capital at near zero marginal cost, thereby generating increasing returns from such investments. Despite being specific to its originator, intangible capital produces large spillover effects. Its characteristics can often be readily copied or imitated because they aren’t always capable of being fully patented. For example, the outstanding success of the iPhone’s design and touch-screen technology led Apple’s rivals first to imitate it, and then to improve upon it. Intangible assets are not always adequately reflected in company balance sheets and in share prices, or in the GDP statistics. It isn’t easy to value intangible assets because there are no ready markets for them.

Businesses can create their own intangible assets. For example, firms can either write down their knowledge of their production processes in lines of code themselves or pay a business development firm to do it for them. The former would be treated as an intermediate production expense, and the latter as an output that would be reflected as additional GDP. But, in both instances, the code would be an intangible capital asset if the software were of enduring value. Such assets can be essential to the productive ability of businesses. For example, some financial institutions are totally dependent on their ageing legacy coding. It is important for the tax system to recognise the vital importance of intangible assets.

Foreign direct investment

Britain has long been the top destination in Europe for foreign direct investment. It offers businesses stable institutions, an excellent legal system, a favourable geographical location, and world-class facilities and highly qualified staff for R&D. Many foreign investors are particularly attracted by the access to the European single market guaranteed by Britain’s (current) membership of the EU. It is unsurprising that there has been a fall in the level of foreign direct investment into the most productive industries since the 2016 referendum. Britain has ceased to be an attractive destination for foreign industrial investment, despite its business-friendly environment. The British economy will acutely feel the loss of foreign direct investment; its economic growth will suffer.

Foreign direct investment tends to boost productivity in the UK by importing capital, new technology, modern work practices and developing skilled managers. Foreign-owned firms tend to be twice as productive as domestic companies, despite using local staff and managers, and being subject to the same rules and regulations. The secret of their higher productivity lies in the fact that they tend to employ more physical and human capital per hour worked than domestic firms. If domestically owned firms increased their physical and human capital to the same level, it would eliminate Britain’s productivity gap.

Why investment matters

The fragility of domestic investment is parlous. Lower investment tends to result in lower productivity and growth, particularly in the manufacturing sector. In contrast, the services sector has continued to grow. High employment, historically low interest rates and low savings have fuelled the buoyancy of consumer spending on services (British households save less than £1 of every £20 they receive in income). The weakened manufacturing sector will drag down growth in the services sector because the two sectors are interdependent.

There has been slower growth in the capital per hour worked (‘capital deepening’) and the efficiency with which companies put their labour and capital inputs to use (‘total factor productivity’) even among highly productive companies. Uncertainty has made businesses reluctant to invest in productive capital, preferring to employ more labour on temporary contracts. Firms can get rid of workers quickly if, as they expect, economic and market conditions worsen. The new jobs are insecure and offer little scope for real wage growth.

Plugging the shortfall

The 2010 Coalition government could have implemented countervailing increases in public investment in the wake of the slump in private sector investment. Instead, it chose to cut public capital investment from 3.4% to 1.7% of GDP between 2009 and 2014. It was politically easier for it to cut capital rather than current spending as part of its austerity measures. In contrast, countries such as Switzerland, Sweden and Denmark maintained their capital public investment at 4% of GDP throughout the recession that followed the financial crisis. They continue to enjoy the highest per capita incomes in Europe. Some economists have argued that the government should use debt finance to increase public capital investment. 'Put bluntly, [increasing] public debt may have no fiscal cost’ (David Blanchflower, former member of the Bank of England's Monetary Policy Committee, 2019).

Public investment projects have a ‘multiplier’ effect greater than one: they pay for themselves. An increase of say, 0.5% of GDP in public investment would lift output by 0.6%. Borrowing to fund public capital investment is ‘good debt’. The Treasury’s National Infrastructure and Construction Pipeline lists some 700 projects ranging from social housing to smart motorways. They would require public capital expenditure of £600bn over the next ten years. But the government is giving scant priority to projects that would enhance productivity growth; for example, the urgent need to extend broadband coverage throughout the country and to improve its speed. The UK ranks 34th in the world broadband speed league table. This is a pitiful rank for a country that has the fifth largest economy in the world.

The government has instead chosen to pour funding into political vanity projects such as HS2. It has also allowed cash-strapped local authorities to borrow vast sums from the Treasury’s Public Works Loan Board (PWLB) to purchase shopping malls and other commercial properties in an attempt to keep open shopping centres in communities that have been ravaged by the growth of e-commerce. The expenditure has bailed out commercial landlords, but it has not added to Britain’s productivity and future growth. Local authorities may come to regret investing so heavily in over-priced commercial property. They were able to do so because the PWLB applies less due diligence than commercial banks, and pays little regard to loan-to-value discipline of capping borrowings to a given proportion of the purchase price.

Unless Britain’s productivity snaps out of the doldrums and picks up, we will need to accept that we are in a new paradigm of lower productivity growth. Namely, there is a permanent impairment to the economy’s productive capacity to grow by at least 2% a year. Optimists argue that Britain is simply suffering from a bad case of a global weakness. And that once the dampening effect of Brexit on uncertainty and business investment is lifted, productivity growth will return to its former trend. Few economists share this outlook.

Research and development

R&D activity stimulates productivity and economic growth. It promotes new technological innovations and encourages their diffusion throughout industry, and the production of new products, processes or services. The government provides substantial support for R&D spending by companies through the tax system (£3.7bn in 2015/16). It also supports spending on the development of new techniques and technologies as a customer, e.g. through defence procurement contracts, and by making grants to universities and research bodies.

R&D activity facilitates experimentation with new products and processes that tend to be a defining feature of commercial innovations. Such experimentation allows firms to assess the commercial prospects of new goods and services before they are brought to market. US data analysis suggests that firms only adopt between 30% and 50% of the new technologies they try, and that about a quarter of new consumer goods for sale are discontinued in the following year.

Wider benefits from R&D

The classical policy rationale for supporting private R&D is the need to address ‘market failure’ because knowledge creation has the characteristic of a public good. Firms cannot appropriate all the external benefits of their investment for themselves through the market because of the intangible nature of knowledge. Basic research would be underprovided in the absence of government support. It creates wide ranging spillover benefits and social benefits for others that are not captured by the market mechanism. Patents cannot fully inhibit the spillover benefits created by R&D activity.

Firms that aren’t involved in the original research can imitate and improve upon the ideas and techniques discovered by the pioneers. For example, most of the technology used inside the Apple iPhone was originally created for the US defence department, including its internet connectivity, touch screen and GPS apps.

Government support for R&D raises the productivity of private and human capital and economic growth, whether the aid is provided through tax relief or direct grants. The introduction of R&D tax credits has resulted in a large increase in R&D spending by businesses. It is estimated that for every £1 of tax forgone as relief, there is an increase of up to £2.35 in R&D spending by businesses. The main advantage of R&D tax credits over grants or subsidies (assuming they are permissible under the EU’s state aid rules) is that they do not involve the government becoming directly or indirectly involved in picking winners. Authoritative studies using data for US manufacturing of the long-run growth effects of public support for R&D have concluded that increasing R&D tax credits increases the growth rate of labour productivity.

Industrial strategy

In 2017, the government put increased expenditure on R&D at the heart of its new industrial strategy. (Britain has had many such plans in the past 20 years.) It has set a target for the government and private businesses to spend 2.4% of the GDP on R&D (the average level of spending by G7 nations) within a decade, an increase in spending by a total of some £7bn between 2017 and 2022. This is an ambitious target: the highest level of spending on R&D prior to 2017 was 1.69% of GDP. According to the CBI, on the trend of R&D expenditure over the past two years, Britain would not be able to meet its target until 2053.

There is no prospect of the government being able to meet its target without a substantial increase in the level of R&D tax credits to stimulate private sector R&D spending. The government also needs to increase its support for research undertaken by universities, public institutes, and on its behalf by businesses under procurement contracts. The increased support would have to be on a sufficient scale to be effective. It would be necessary to have safeguards to ensure good value for money. Ministers would need to accept that there is a potential risk of failure with all R&D activity. But this would be the most productive and least controversial form of public expenditure.

There is also a powerful case for the introduction of a tax break for encouraging increasing business investment in intangible capital. It could be modelled, for example, on the Singapore government’s productivity and innovation tax credit. This covers expenditure not just on R&D activities, but also on design, automation of processes, training and the acquisition and development of intangible assets.

Strengthening innovation infrastructures

The government has taken a leaf out of Germany’s book to create a new innovation infrastructure by establishing catapult centres. They are modelled on Germany’s Fraunhofer Institutes, which support innovation and its diffusion to German companies. For example, the high value manufacturing catapult bridges the ‘valley of death’ between technology ideas and preparing products for the market (‘commercialisation’). It delivers £15 for every £1 of government investment. There are currently ten catapults with a staff of 1,500 employees and an annual budget amounting to 0.01% of GDP. They support around 600 smaller companies each year.

There is a strong case for a rapid and large increase in the number of catapult centres. Germany now has more than 70 Fraunhofer Institutes, employing almost 25,000 people and helping around 6,000 to 8,000 large and small companies each year. They have an annual budget of a little under 0.1% of German GDP. The government should also seek to emulate Germany’s Steinbeis Enterpises. Created in 1971, it is a network of about 6,000 technical professional staff that operates through a thousand enterprises. Companies across Germany can draw on their knowledge, skills, experience and know-how.

Productivity and human capital

Human capital, namely the education and skills embodied in the work force, is one of the most important determinants of labour productivity. Britain is less productive than other advanced nations because much of its labour force lacks the skills required for a productive, competitive and growing economy. Even as a high employment and low productivity economy, it will be increasingly difficult for Britain to continue growing simply by drawing more people into the labour force. It has an ageing population, and the uncertainly over Brexit has reduced the former ready availability of skilled labour from the EU.

Britain spends more money than most countries on education, but its spending on training per employee is little over half the EU average. Britain tends to lag behind the EU and its other trading rivals on literacy, numeracy, digital skills and workplace training. There has been a substantial and long-term decline in the volume of employer training and investment in training because of the trend towards high employment and low skill service business models.

The apprentice levy is a 0.5% payroll tax on businesses with an annual pay bill of £3m or more. Employers receive vouchers in return for the tax they pay. The vouchers must be used within two years on approved training courses. The government introduced the apprenticeship levy in 2017 in an effort to reverse the long-term trend of employer under-investment in training. It was supposed to improve productivity by increasing the quality and quantity of apprenticeships. But, in fact, the number of good quality new apprenticeships has declined since the introduction of the levy.

The scheme is highly inflexible. For example, a million workers on temporary contracts are not eligible to join the scheme, even though the recruitment agencies that provide their services contribute about 5% of the yield from the levy. Agency workers play a key role in filling in during peak periods of demand. They help to transfer new skills as they move between assignments. They don’t qualify for support because of the rule that an apprenticeship should last at least a year. The apprentice levy is intended to fund training for workers with low skills, but some employers are using the levy to fund degree level courses, including MBAs. It does not provide funding for shorter training courses, e.g. on digital skills, even for staff who are low skilled.

The CIPD has pointed out that the levy will only boost overall investment in training if it doesn’t lead to the government subsidising training that is currently being funded by employers, the displacement of other training, or the rebadging of existing training activity. The CIPD has criticised the quality and narrowness of the off-the-job training provided. It has made a case for a broader training levy. The apprentice levy covers only around 2% of employers. It goes only a small way towards increasing spending on workforce training to the level in other advanced economies.

There is a dissonance between the skills that the government says it wants workers to acquire to serve the economy, and its policy on higher education and skills training. The government has over-expanded the higher education sector at the expense of skills and vocational training provided by further education colleges. Less academic students now increasingly choose to attend marginal universities to read for ‘Mickey Mouse’ degrees, in preference to acquiring workplace skills that would equip them for employment. They often leave university with practically worthless degrees that aren’t valued by potential employers, and saddled with lifelong debts.

At the same time as it has increased the number of students in higher education, the government has reduced funding for further education colleges and cut their student numbers. Even though further educational colleges specialise in providing training in trades, applied science, technology, engineering and mathematics: the very skills that boost labour productivity.

Developing a skilled workforce

Britain will not be able to increase its productivity growth to its former level, let alone increase it until it ramps up skills training to equip its workers to meet the needs of a competitive modern economy. For example, England currently has a larger proportion of low-skilled young workers than most of the rest of the OECD. And worryingly, its younger workers tend to be no more skilled than the older ones. Workers with little or no skills, who are the most in need of training, are often resistant to acquiring workplace skills. (The most enthusiastic consumers of any training provided by employers tend to be employees who already possess higher or further educational qualifications.)

If the government is serious about addressing low productivity, it should ensure that low skilled workers receive the training they need to become more productive. It should begin by restoring the budgets of institutions of further education (IFE). IFEs provide the vocational and skills training that businesses need to grow. The government should encourage national and local employers to work with IFEs in designing and delivering skills training by seconding professional staff. It should raise the profile of vocational qualifications by offering bursaries, grants and subsidised fees for those attending courses in the subjects most in demand by employers.

There is also a case for offering tax incentives to employers who encourage staff of all ages (not just those below the age of 21 years) who currently have low education or training to acquire practical skills and qualifications through sandwich courses and national diplomas. The government should also explore using the tax and benefit systems to encourage more school leavers and workers to acquire qualifications through sandwich courses and national diplomas, such as higher national diplomas (HND) and higher national certificates (HNC).

The fourth industrial revolution

The widespread diffusion of robots infused with artificial intelligence (AI) will offer businesses substantial scope for increasing productivity. Orders for industrial robots have increased three-fold over the past decade, and private equity invested in AI has doubled over the past year. Autonomous robots have a clear edge over human workers. They are stronger, cleverer, learn more quickly, and keep going longer. They don’t need pay, holidays, lunch breaks, tea breaks, and never go on strike or repeat mistakes. For example, the annual cost of operating a robot welder is about a third of what it would cost to hire a human welder.

Digital and AI-robotics are daily opening up productive opportunities and possibilities for advanced economies. The OECD has warned that the spread of AI infused robotic technology will transform economies and radically change people’s jobs and careers. Some 14% of existing jobs could disappear in the next 15 to 20 years, and a further third will face a significant risk of change. This mass displacement of workers will occur unless human capital deploys and leverages the new technologies wisely, to create new and better quality jobs for workers.

Otherwise, the surge in productivity they create will exacerbate income and wealth inequality. The benefits will accrue to the small number of workers in productive industries that retain their jobs, and to the owners of the businesses that create or adopt the new technologies (or both).

There tends to be a lag between technological breakthroughs and surges in productivity, but practically every worker will face a technological challenge to their continued employment at some point in the future. The government, businesses and educational institutions need to work together to address the challenges facing the economy. In particular, to prepare workers and future members of the workforce by encouraging them to engage in lifelong learning to prevent the depreciation of their skills, facilitate movement between roles, and mitigate the risk of obsolescence.

Amazon is one of the most technologically advanced companies in the world and a pioneer in deploying AI-robotics. It has risen to the challenge posed by AI-robotics by recently announcing its intention to retrain a third of its US workforce to address the impact of automation. Some of the workforce will be retrained for higher-skilled work, but Amazon has made it clear that others will need to move into careers outside the company; they will no longer be required. While Amazon’s profits and share price have rocketed, its workers have not benefitted to the same extent from the prosperity created by its transformational productivity growth: the median wages of its employees last year were a modest $28,836.

Labour Party proposals

In 2018, the Labour Party said that if it wins the next election, it would maintain the Bank of England’s operational independence, but widen its mandate. As part of its plan to overhaul Britain’s ‘economic architecture’, it has said that it would make the Bank responsible for increasing productivity growth in Britain to 3% a year. The Bank would be expected to influence the growth of productivity by steering commercial banks into lending to companies engaged in manufacturing and high-technology activities, particularly in the regions.

The Labour Party has also proposed the establishment of a Strategic Investment Board, and transformation of the RBS into a national investment bank to focus on lending to businesses operating outside London and southeast England. It has consistently argued that too much funding is poured into speculative financial and property transactions.

Under the proposed policy, the government and the Bank of England would enter into an agreement to work together to achieve the target. After each Budget, the Bank would be required to report on the government’s plans. The Bank’s current role is to use its power to set interest rates to control inflation, and to maintain financial stability. Monetary policy cannot alter the productive potential of the economy. The quality, knowledge and skills of the labour force and the level and efficiency of investment determine productivity, real wages and living standards, not the money supply and interest rates. Critics of the proposed expansion of the Bank’s remit have pointed out that, despite the efforts of successive governments, Britain has never previously sustained a productivity growth rate of 3%.

Embroiling the Bank in directing commercial lending would involve it in ‘picking winners’, a role for which it is not equipped. Making it responsible for stimulating industrial productivity would be a dubious addition to its current responsibilities. The Bank has maintained a diplomatic silence about the Labour Party’s proposals. But its likely views can be gleaned from what Mark Carney, the governor of the Bank, said in 2017 about those who wanted the Bank to deliver lasting prosperity by solving Britain’s chronically ailing productivity performance. He said that they ‘confuse independence for omnipotence’.

Need for a longer-term focus

The economy remains dominated by consumerism fueled by economic myopia: a shortsighted view of the future. Britain currently has the lowest level of personal saving in 60 years. Businesses that wish to invest and grow need long term finance, ideally in the form of equity capital. Businesses that don’t succeed in raising finance often blame it on the stock market’s alleged ‘short-term mentality’. They say that the City is more focused on the quarterly results of listed companies and speculating on daily fluctuations in prices of shares, currencies and other financial assets than in supporting industry. They cite Keynes’s (1936) observation that: ‘Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation. When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill done’. This critique overlooks that the City’s reluctance might be due to the potential borrowers’ expected lack of profitability or independent management.

Britain’s future prosperity depends on a revival in its productivity growth. The political and economic uncertainty surrounding Brexit is causing businesses to postpone investing for the future, or to invest abroad until political stability is restored. The impact of the uncertainty will linger for years. In the meantime, investment, productivity, growth and living standards will stagnate. The Bank of England has lowered its forecasts for economic growth, even those based on the assumption that Britain will leave the EU with a deal. The productivity of the British economy will not improve without a substantial and sustained increase in public and private sector investment and R&D spending, and in the skills of its workforce.